As we enter 2022, we remain confident that the conditions are right for a significant turn in the Value-Growth cycle. 2021 was mixed, with a few false dawns for Value, but Value ended the year (again) lower, compared to Growth, and at about the same level as the trough in Fall 2020. This marked the fifth consecutive year of Value underperformance, during which time, relative to growth, Value has lost about half of its value (i.e., a 50% cumulative relative decline, using the Russell 1000 Value and Growth indices).

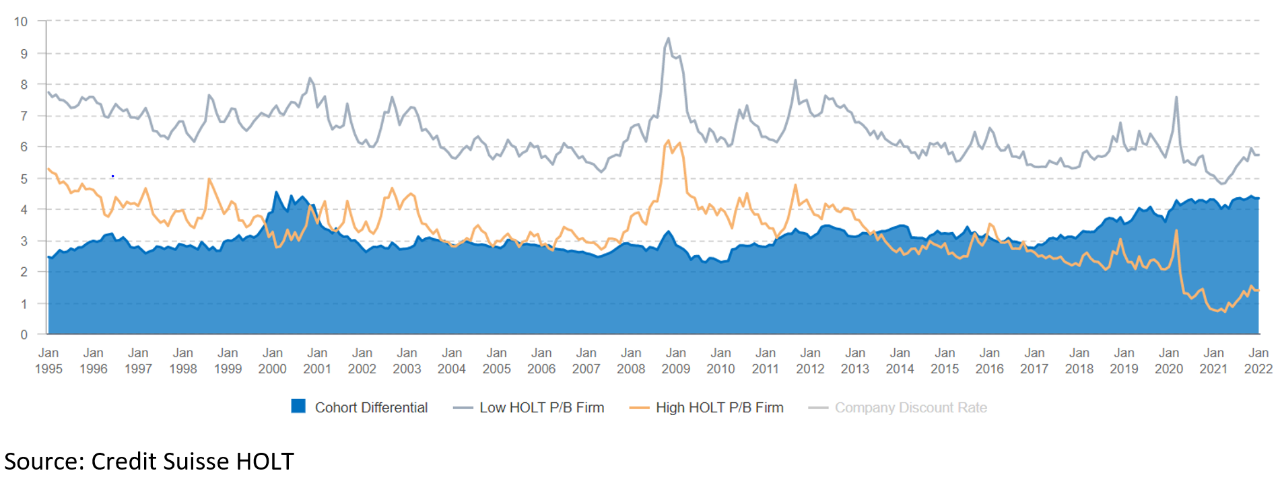

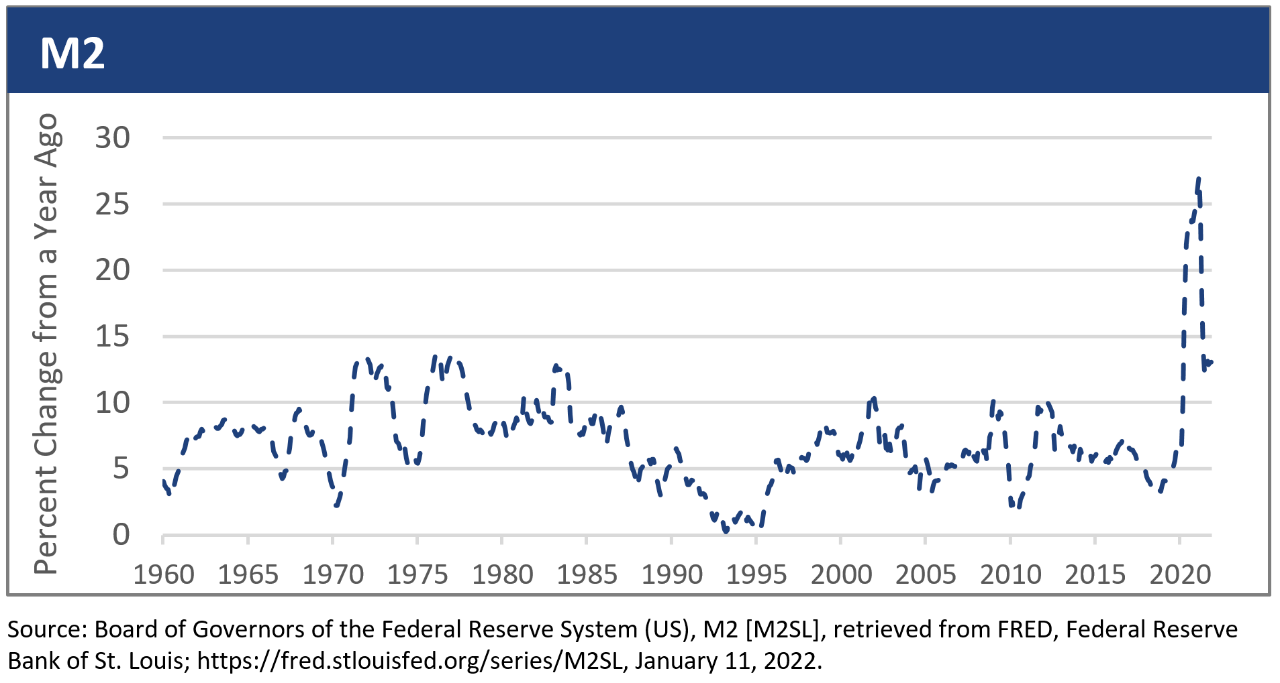

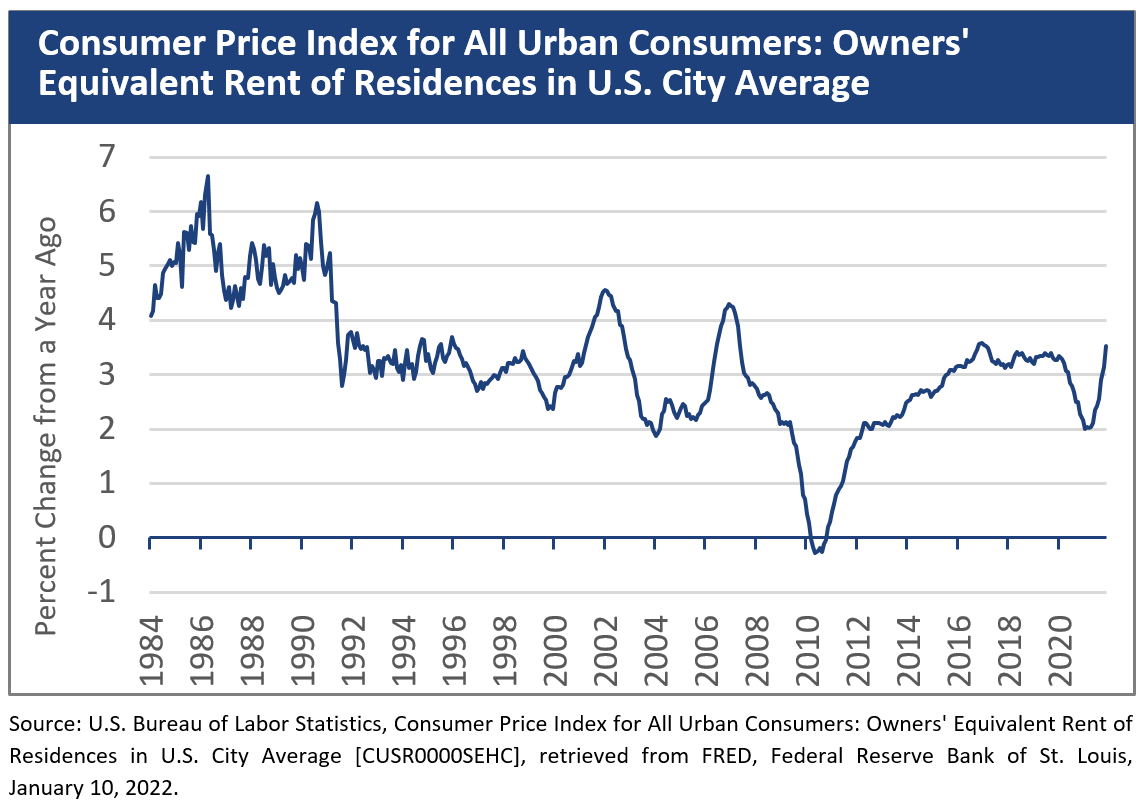

We believe the conditions are right for a few reasons, namely, higher inflation, higher real interest rates (i.e., less-negative real interest rates), and what we feel are clear signs of excessiveness in Growth/Momentum sectors’ valuations. The relative payoff to Value, we think, can be very significant, given valuation differentials between Value and Growth are at essentially the same levels as the Internet Bubble of 1999-2000. That combination (better-than-average probability and higher-than-average payoff) is compelling, and the definition of an attractive risk-reward.

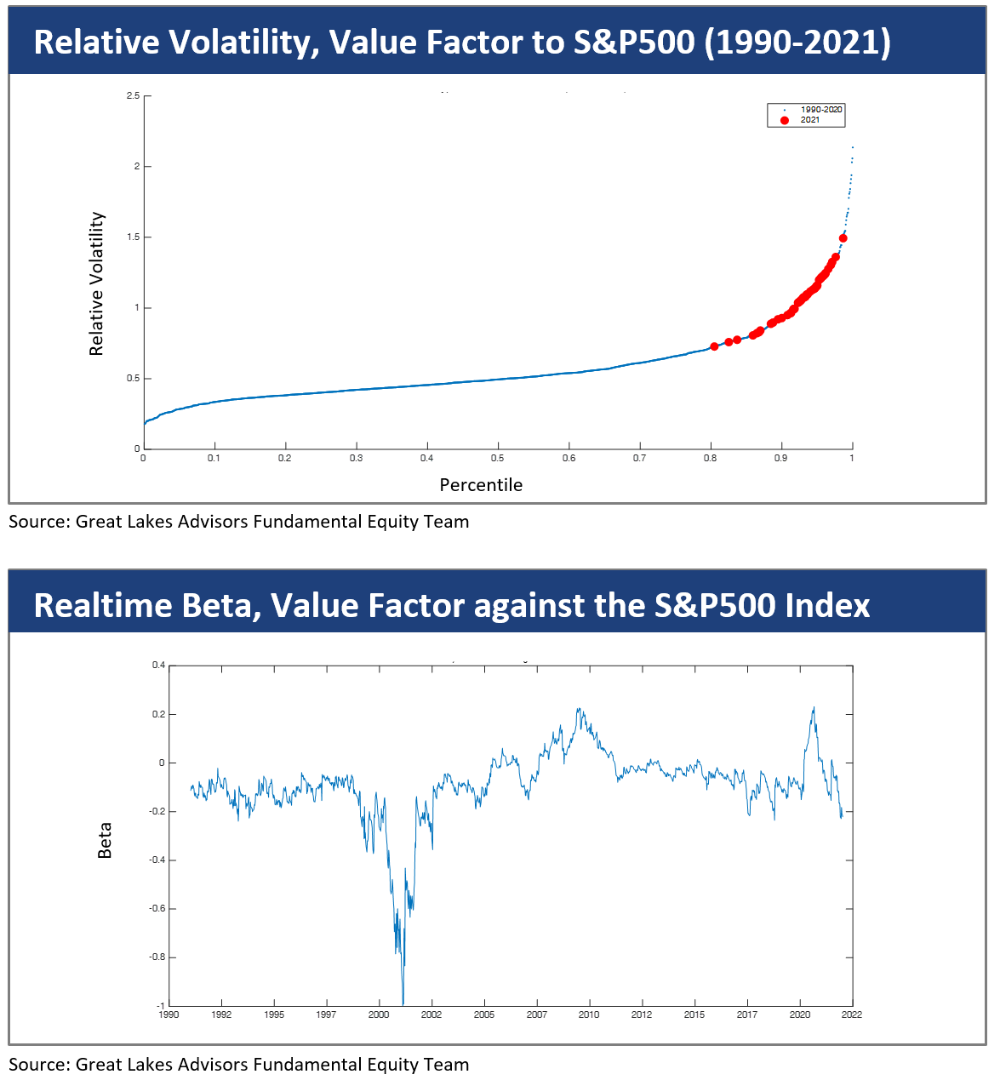

Volatility has been very high, and that’s not uncommon around inflection points. The top chart below shows the relative volatility of Value to the overall market, and the latter is the “realtime” beta of Value to the market. Each shows 2021 as anomalous, rhyming in many respects to 1999-2000. The relative volatility of Value in 2021 was more than double the long- term average, and eclipsed only by a few weeks in 2000. Value’s beta has compressed to sharply negative, a welcome development in our view, and rightly reflecting a much lower risk profile for Value stocks, when compared to a very expensive and vulnerable broader market. And the most negative since…1999-2000.